Foundation Homes

Quality new construction, guided from start to finish. Purchase your lot, build below market value, and move in with real equity.

Quality new construction, guided from start to finish. Purchase your lot, build below market value, and move in with real equity.

Each design is priced with transparency. Pick the one that fits your life and budget.

*All pricing is estimated and assumes a specific lot cost. Actual costs vary based on lot, site, and finish selections.

New designs are in development. Check back soon.

Estimated figures based on $25,000 lot, 7% interest rate, current Bella Vista tax rates, $45/mo POA, and $150/mo insurance. Actual costs vary. Not financial advice.

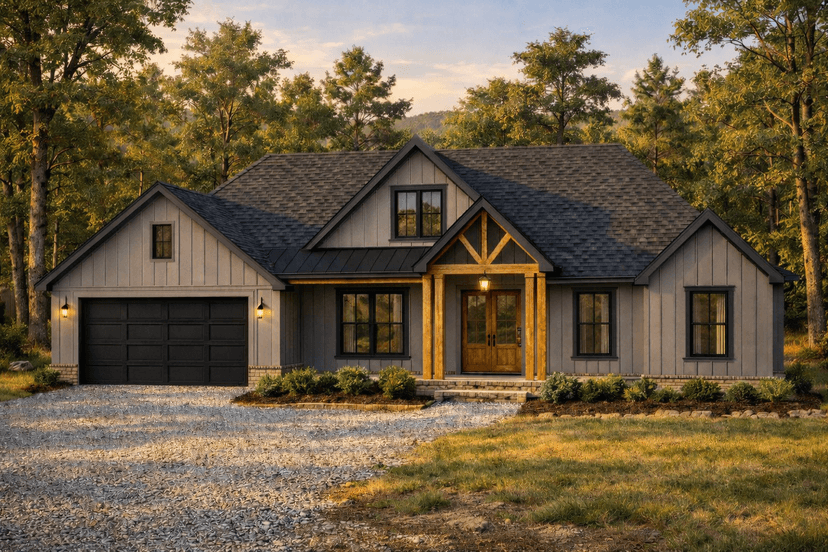

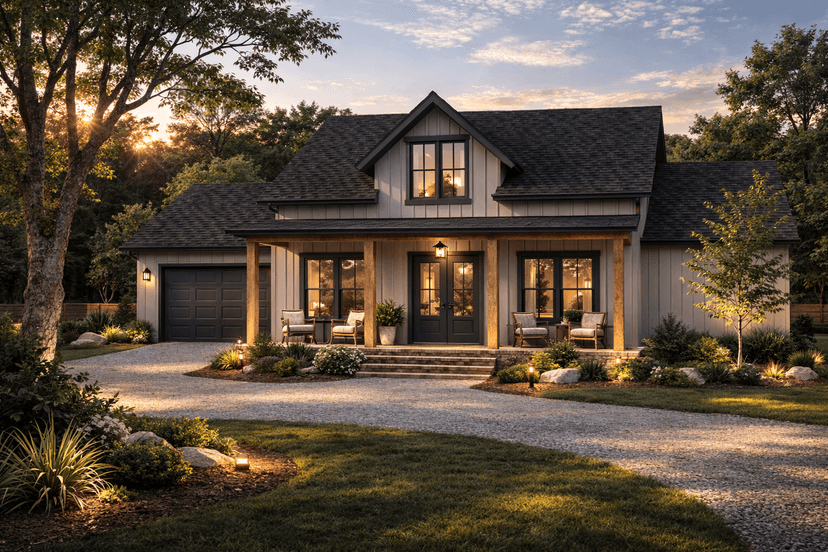

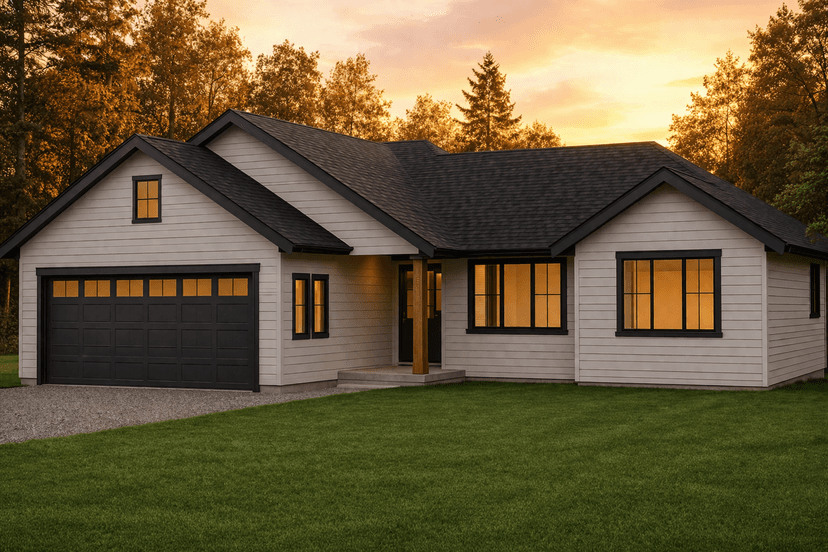

| Proto | Heritage | Vista | Apollo | |

|---|---|---|---|---|

| Size | 996 sqft, 2/2 | 1,479 sqft, 3/2 | 1,515 sqft, 3/2 | 1,889 sqft, 4/2 |

| Total cash | ~$39,500 | ~$45,000 | ~$45,500 | ~$50,800 |

| Instant equity | $40,726 | $56,561 | $60,027 | $81,616 |

| Monthly payment | ~$1,717 | ~$2,443 | ~$2,498 | ~$3,052 |

| Appraised value | $245,000 | $335,000 | $345,000 | $434,470 |

Estimated figures based on $25,000 lot, 7% interest rate, current Bella Vista tax rates, $45/mo POA, and $150/mo insurance. Actual costs vary. Not financial advice.

Northwest Arkansas offers something rare: natural beauty, growing opportunity, and a strong sense of community. Our homes are designed to fit this lifestyle.

Over 100 miles of trails, multiple lakes, and outdoor recreation minutes from home.

Neighbors who know each other. Local events. A pace of life that makes sense.

NWA is one of the fastest-growing metros in the country, with strong job growth and opportunity.

From first conversation to move-in day, we guide you through every step.

We start with a conversation about your goals, timeline, and budget. No pressure, just clarity on what's possible and what it will cost.

Browse our home designs. Each plan shows total cash required, estimated monthly payment, and the equity you'll have at move-in.

We help you find and purchase the right lot in Bella Vista. You buy it with cash ($25,000), along with the Themelios initial deposit ($5,000) and soft costs for pre-construction due diligence ($5,000).

Phase 1 Cash: ~$35,000

We submit your plan to the city for permits. During this time, you keep living where you live. No payments, no construction activity. Just waiting for approval.

6-8 months

With permits approved, your construction-to-permanent loan closes. Your lot equity covers most of the down payment and closing costs. You fund an interest reserve for payments during the build.

Phase 2 Cash: varies by plan

Your licensed builder constructs your home. You receive regular updates and milestone notifications. Interest-only payments are made from your funded reserve.

6 months

Your loan converts to a 30-year fixed mortgage. You own a brand new home with real equity built in from day one.

Wake up to trails, lakes, and a community that feels like home. Build wealth with every payment. Manage everything through your Foundation OS (coming soon). Warranties, maintenance, and more.

When you buy an existing home, your loan is based on the market price of the house. That price includes 10-20% margin baked in by the builder or previous seller. You are financing their profit.

When you build with Foundation Homes, your loan is based on the actual cost to build the home, not the market price. The finished home appraises for significantly more than it cost to build. That gap between what you owe and what the home is worth is your instant equity.

Here is why the gap matters over time: a 30-year mortgage is amortized so that your early payments are mostly interest. Very little goes toward paying down the loan balance. A conventional buyer who puts 10% down has to make years of payments before their equity grows meaningfully beyond that initial down payment.

A Foundation Homes buyer skips that slow start entirely. You move in with 17-19% equity already built in. A conventional buyer would need 6.2-7.6 years and $113,000-$236,000 in mortgage payments just to reach the equity position you had on day one.

The tradeoff is time. Foundation Homes takes roughly 14 months from lot purchase to move-in (6-8 months permitting plus 6 months construction). If you are willing to wait, you start with a permanent financial advantage that no conventional purchase can match.

Heritage plan, side by side: building with Foundation Homes vs. buying the same home at market price.

A conventional buyer would need

6.2

years

$150,000

in mortgage payments

to reach the equity position a Foundation Home buyer has on move-in day.

Based on Heritage plan. Estimated figures, actual results vary.

Buying an existing home often means compromises: outdated layouts, deferred maintenance, or paying a premium just to get into the market. And in a competitive market, you might lose multiple offers before finding something that almost works.

New construction changes that equation. You get a home built to current codes, with modern systems, designed for how people actually live today. No guessing about what the previous owner left behind.

6-8*

months typical build time

1 yr

builder warranty on workmanship

17-19%

instant equity built in at move-in

*Construction timeline upon approved permits. Does not include permit approval time.

Foundation Homes is built for people who are willing to trade time for a permanent financial advantage. Dual-income households earning $80,000-$170,000 with $40,000-$52,000 in savings or accessible equity. First-time buyers who want to start with real equity instead of years of payments to break even. Existing homeowners who can tap a HELOC to fund the lot while they build their next home. Patient buyers who understand that 14 months of building creates an advantage no conventional purchase can match.

Every mortgage payment builds ownership. Over time, your home can become a foundation for your next chapter, whether that's staying put, upgrading, or something else entirely.

Year 1

~$347k*

estimated home value

Year 5

~$407k*

estimated home value

Year 10

~$496k*

estimated home value

*Illustrative example based on the Heritage plan at $335k appraised value with 3.5% annual appreciation. Your equity is the difference between home value and remaining loan balance, which depends on your financing terms. Not financial advice.

Ready to see if Foundation Homes works for you? Schedule a call. We will walk through the numbers for your situation.